Why Waiting to Buy Can Cost You

Rent increases every year. A fixed mortgage payment doesn’t. The national average rent increase is around 5% annually (Monarch/Realtor.com, 2026), which means a renter paying $1,800 a month today is likely paying $2,300 by year five — for the same apartment. A fixed-rate mortgage taken out today has the same principal and interest payment in year five and ten years that it had in year one.

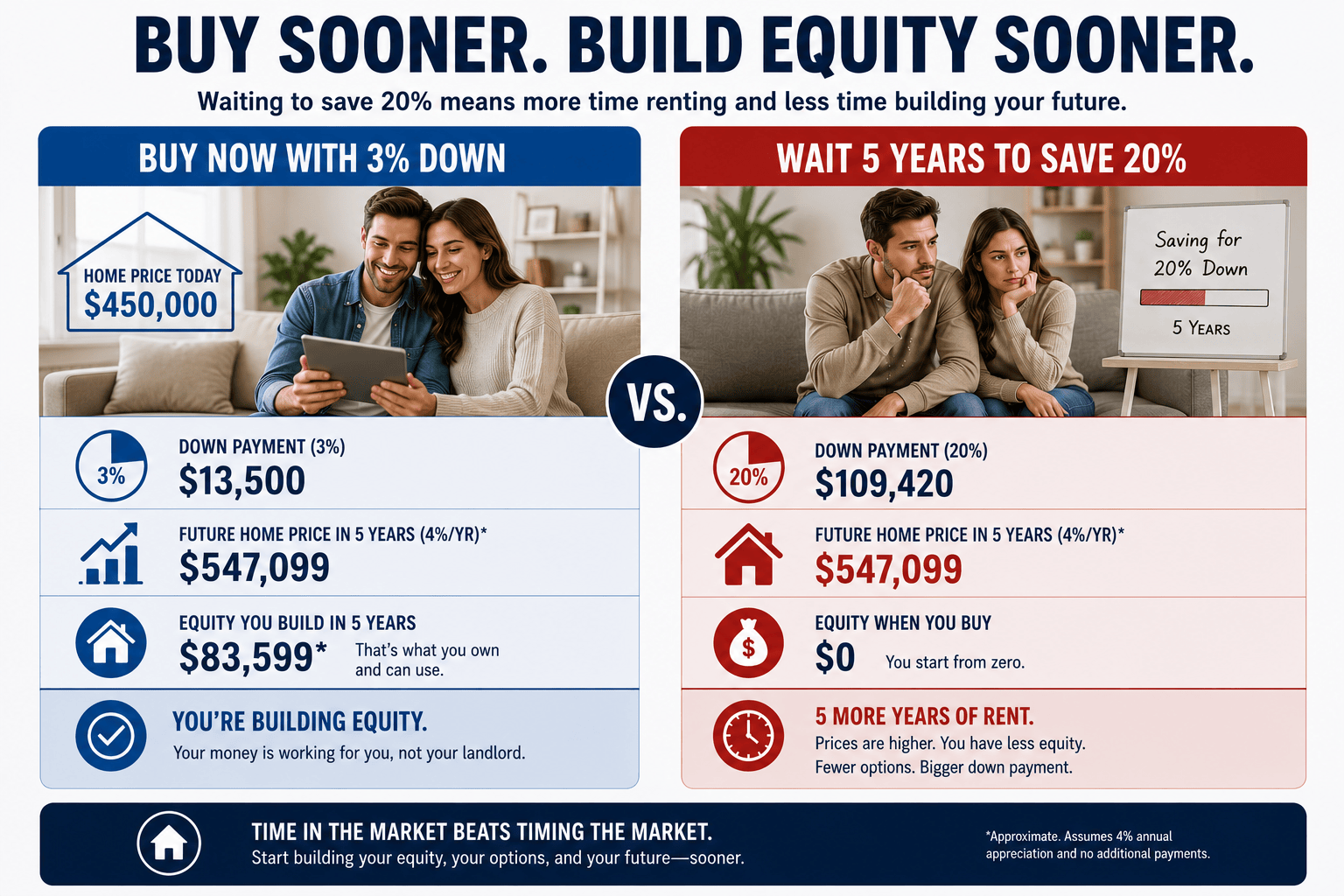

That difference compounds. Every year spent renting is a year of housing costs with nothing accumulating on the other side. No equity, no principal paydown, no appreciation. On a $400,000 home, five years of ownership typically builds $80,000 or more in equity through principal paydown and modest appreciation. Five years of renting builds zero for you.

The wealth gap this creates over time is significant, even if you have to move for work or life choices every 7 to 10 years. Over time, it adds up.

The Federal Reserve’s Survey of Consumer Finances puts the average homeowner’s net worth at 40 times that of the average renter. That number is the result of years of mortgage payments that build ownership stake while rents keep climbing.

I know you might be thinking, but Ramsey has you wait so you pay less interest in the future. Is that your reality? When can you afford nearly 2X the payment (15-year vs a 30-year fixed), be debt-free, and save 20% down? That isn’t the right way to think about it, because you are wasting rent and not accumulating wealth while waiting. It’s not free to wait. And getting started positions you to have the 20% down payment for your next house in 7-10 years through appreciation.

Timing the market is another concept that costs would-be buyers, because emotions shouldn’t rule the day — assessing the bottom line should.

When rates dropped sharply in 2020, home prices surged. Buyers who jumped in then rather than the year before when rates were two points higher found themselves with stiff competition to even win a house much less not pay over-asking. In short order, the most qualified buyers drove up the market, making a fortune for those who bought prior.

Things have cooled off, so that window has passed for now. But national appreciation over the past 70 plus years tells us that you can expect housing to appreciate at 3-4%, which on an asset that is hundreds of thousands of dollars, is the value of leverage. What would your same down payment have done for you in the bank? These are the questions to ask yourself.

The housing market remains strong: housing supply is still 3 to 4 million units short of demand nationally, and home prices are projected to rise 2 to 5% in 2026 regardless of what rates do (NAR; Zillow; Redfin, May 2026). Waiting is not a neutral position — the market moves while you’re watching it.

The final piece is payment reality. In most markets right now, a mortgage payment on a starter home is close to comparable rent. Some markets are significantly less, but only a few are nominally more. The average U.S. rent sits at approximately $1,850 per month as of mid-2025 (Zillow, 2025), while mortgage payments at current rates on modestly priced homes fall in a similar range depending on down payment and location. Regardless, there are tax benefits to help, and you are buying leverage which your rent doesn’t do.

None of this means buying is the right move for everyone right now. Not at all. Timeline, financial readiness, your career stability, and local market conditions all matter. But for buyers who can afford a 30-year fixed with low down payment and plan to stay put for five or more years, the cost of waiting is real, and it grows every year.